Explore the first practical trust use cases for your bank

Topics include; onboarding and customer verification, digital enrollment, high-risk transaction authorization and trust modernization in existing digital journeys.

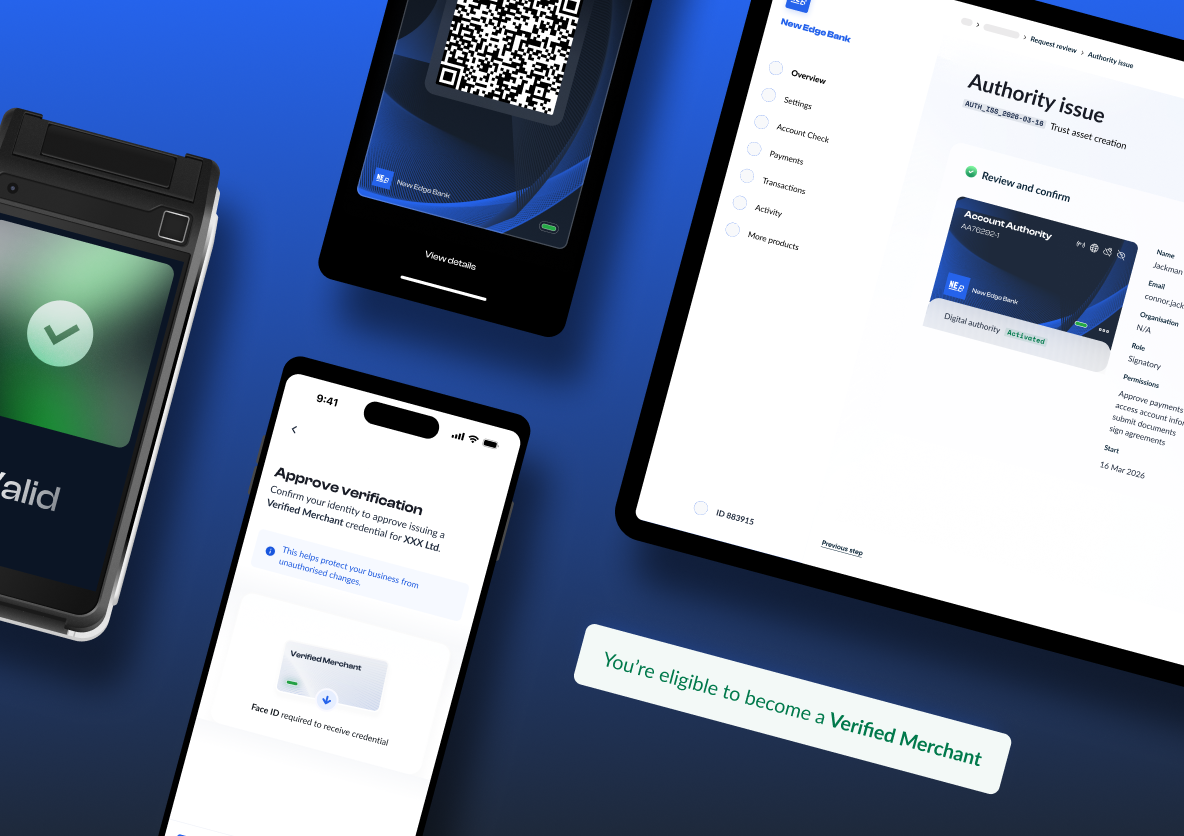

Improve onboarding, enrollment, and high-risk authorization with stronger digital trust signals — and reduce the cost of repeated verification across the customer lifecycle.

Banks are under pressure to solve harder trust problems inside the journeys they already run. Across onboarding, enrollment, recovery, and high-risk transactions, trust is still being rebuilt again and again — increasing cost, creating friction, and weakening confidence where it matters most. This isn’t a lack of identity verification. It’s a lack of trust continuity.

At the same time, expectations are rising. Digital channels are now primary, fraud is targeting weak points in trust, and stronger digital trust signals are becoming more usable in real workflows.

That creates a clear opportunity:

Improve the journeys you already operate by introducing stronger, reusable trust signals — reducing the need to start from zero every time.

Many current bank workflows still rely on a familiar mix of:

Document capture

Repeated identity proofing

Fragmented exception handling

Channel-specific controls

Disconnected records for audit governance

This creates a predictable outcome:

higher operational cost, more customer friction, and weaker confidence in the moments where risk is highest.

Banks have an opportunity to improve the workflows they already operate by introducing stronger, reusable trust signals.

This means:

→ Fewer repeated checks

→ Better continuity between onboarding and digital access

→ Stronger support for high-risk decisions

→ Better use of trust already established earlier in the lifecycle

Most banks already have identity verification. The problem is that trust does not carry forward. Acceptance-first is about improving how trust works across the lifecycle:

→ Stronger onboarding trust

→ Better continuity into digital access

→ Better support for high-risk decisions

→ Fewer repeated checks

→ A stronger foundation for broader trust and modernization

Waiting keeps banks locked into repeated verification, growing exception-handling overhead, and brittle controls in trust-heavy journeys. Banks that move earlier can improve live workflows now, create cleaner trust continuity across channels, and establish a stronger base for broader digital trust adoption over time.

A good acceptance-first strategy starts with one workflow, not a full transformation.

Choose a trust-heavy journey

Identify where repeated checks or weak controls are creating pain

Introduce stronger digital trust signals in that workflow

Measure improvement in fraud, friction, or efficiency

Extend the model once it works

Public guidance is beginning to converge around practical bank use cases for stronger digital trust. Recent guidance highlights workflows such as:

Account application

Digital enrollment

High-risk transaction authorization

That does not replace a bank’s own architecture, risk, or compliance decisions. It does make the conversation more practical and easier to prioritize.

MATTR was an active collaborator in NIST/NCCoE’s mDL project, which demonstrates how mobile driver’s licenses can support secure, standards-based digital identity use cases for financial institutions. MATTR contributed verifier and wallet technology, including MATTR VII and Kakapo Wallet, and MATTR team members helped build the demonstration lab environment documented in the draft publication.

Topics include; onboarding and customer verification, digital enrollment, high-risk transaction authorization and trust modernization in existing digital journeys.